What makes Japanese GX-ETS different?

- Jun 9

- 4 min read

Japanese GX-ETS has entered full operation from 2026. The fundamental structure of GX-ETS is just like other compliant cap-and-trade carbon market. Companies with obligation should report their emissions and trade for their allowance deficiency or surplus. However, there are distinct features of GX-ETS making it stand out as a more corporate-driven approach. Companies should be aware of these distinctions and the reason behind to make carbon pricing less of a burden and more of a strategic input.

Emission allocation – To use a bottom-up approach

In a traditional ETS, when emission allowances are allocated to companies, it is companies who submit firstly their emission-related data to responsible agencies and the agencies who will then determine the number of allowances allocable using different approaches such as grandfathering or benchmarking. However, in GX-ETS, the calculation of allowances allocable falls into the hand of companies (following parameters set by government). This process is realized by the companies’ submission of a so-called “emission target” to the Ministry of Economy, Trade and Industry. Looking to the GX-ETS schedule in Figure 1, the “emission target” (point 3) will be submitted before the end of September of the compliance year, after which the emission allowance will be approved and allocated to each companies.

(Translated from GX-ETS leaflet published by METI)

In this way, companies are given the transparency of the benchmark, i.e., the efficiencies in terms of emission intensity in their industries and will be aware of the speed they should be driving their emissions down. This is somewhat similar to baseline-and-credit approach adopted by GX-ETS in its 1st voluntary phase, where companies set their own baseline emission reduction targets and pathway, and can be credited if achieve better reduction performance than the baseline. Companies are designated to be more actively engaged in the decision of emission reduction instead of a mere game of allowance of “allocation and submission”.

However, this also means that the underlying burden of data collection and calculation completely lies on companies. They also have to acquire full knowledge on allowance calculation method as recorded in calculation manual published by the government. This would bring heavy human resources and time effort, or financial cost if outsourced to service provider.

Transition plan – To plan for emission reduction investment

In alignment with the bottom-up approach of determining allowance calculation, companies are required to submit their “transition plan” (point 4 in Figure 1) to METI. The transition plan includes five sections:

- CO2 emission in the previous year

- Target of CO2 emission until 2030

- Plans of investment in activities related to the transition toward decarbonized economies (e.g., equipment upgrade)

- Plans of investment in R&D related to the transition toward decarbonized economies

- Other matters

The requirement of submission of “transition plan” results from the exact same reason why the responsible of allocation determination is passed to companies, that-is to explicitly drive companies to compare the cost of self-decarbonization investment and that subject to ETS regulation, and to foster decarbonization effort rather than passively respond to allowance deficiency. The procedures can be summarized in Figure 2.

As can be observed in the chart, these elements fundamentally serves as the input of an analysis of carbon pricing, at least for decarbonization activities. The analysis is necessarily subject to various uncertainties including allowance prices variation, emission and output forecast, technologies and policies update, but it can inform companies’ investment decisions at primary stages. Meanwhile, government can also make use of these input to adjust their ETS correction measures and revise emission reduction trajectory accordingly.

Conclusion

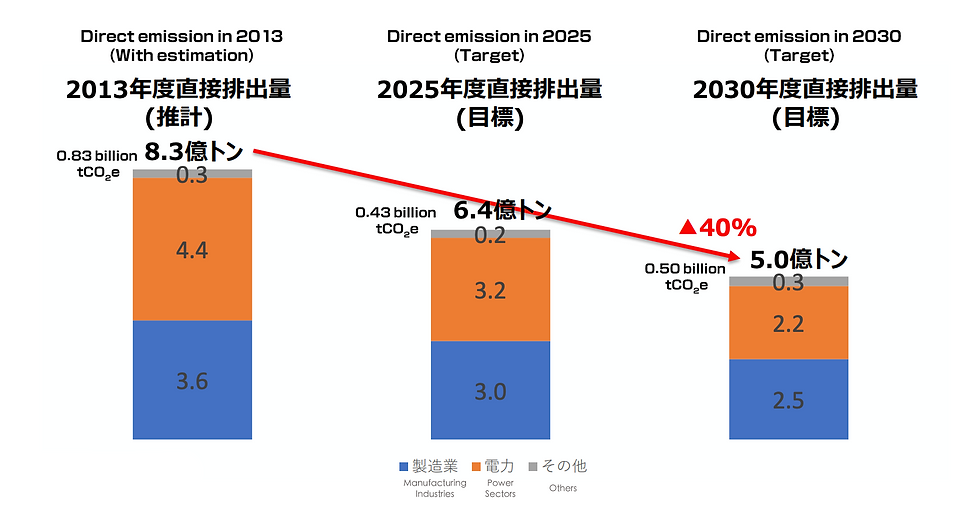

Nonetheless, as can be shown by the outcome of 1st phase of GX-ETS (Figure 3), a completely corporate-led target-setting approach is not likely to be sufficient (Japanese NDC, as a benchmark, targets 32.4% and 46% of emission reduction in 2025 and 2030 respectively with 2013 as base year to achieve carbon neutrality in 2050). Therefore, government should still play its role in GX-ETS to keep emission reduction pathway aligned. As a result, GX-ETS has chosen to integrate two approaches in pursuit of a more achievable decarbonization in its 2nd phase.

To sum up, as Japan introduces its formal rules of compliance carbon markets and unique corporate-driven approaches, companies are swiftly pushed to account for carbon pricing compliance in their decarbonization effort, with a higher ambition. What companies are suggested is to rapidly adopt a series of measures including:

Receive proper training and education for a good understanding on the functioning of GX-ETS and its allocation methodological ideas, and resort to external expertise if necessary

Integrate carbon compliance cost internally into companies decarbonization strategies and refer it as a benchmark for internal carbon pricing so that submitting the transition plan should not be an individual “reporting ”effort

Be timely aware of carbon market and policies update that may have an impact on companies decarbonization investment decisions

Reference:

Comments